Going by the number of mobile phone subscribers, India has become the world’s fastest growing region. Cellular mobile services were introduced in India in August 1995. The initial growth was lacklustre. Subscribers were added at the rate of 0.1 million per month at best for the first 5-6 years. In August 2007, 8.31 million subscribers were added. In May 2006, subscription crossed the 100 million mark. By September 2007, it had doubled. The accelerating pace of this industry in India is clear. This growth has outpaced all predictions. Some predicted 100 million by 2007 and 200 million by 2010. Now the estimate is 500 million by 2010.

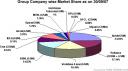

Although cellular networks were introduced in India 7 years later than in China, India’s growth has overtaken China’s in the same time frame since inception. A chart (Figure 1) taken from India-cellular.com reflects the market share of the main players as of September 2007. Of the 204 million subscribers (TRAI quotes a figure of 209 million [1]), 75% were in GSM and the rest in CDMA. The four Metros accounted for 19% of the market.

Figure 1

With an estimated population of 1.136 billion and about 72% living in rural areas, we can estimate that the urban population is 318 million. Given that only 2% of the rural population have access to mobile phones (16 million) [Gartner Research], the next growth segment is in the rural areas. This implies an urban penetration of 92%.

Table 1

What I found to my great surprise was wireline connections when compared against wireless. Table 1 released by TRAI on 22 Oct 07 tells us the impact of wireless [1] . Wireline compares feebly against it. We can infer many things from this table and associate some reasons for the growth of wireless.

- Since wireless has only marginal penetration, we can infer that wireline connections to rural areas are quite low.

- Capturing the rural market will never make business sense by laying down copper wires. Going wireless is the way.

- A typical urban household has one mobile phone per person (best case) whereas only one landline per household. This accounts for the much higher wireless subscriptions we see.

- Given the comparable pricing of wireline and wireless connections, and the added advantage of mobility that wireless brings, people are switching from wireline to wireless.

- Wireline has a fixed monthly rental charge. Wireless has this but more importantly the ability to offer prepaid service which works out cheaper for many income groups.

It’s worthwhile to look at some of these issues in some detail.

Urban areas are generally well connected by copper. Many people, especially among the retired and elderly, have been slow to change from their wired connections to wireless. This too is set to change as owning a mobile phone becomes cheaper than a landline. The competition among cellular operators and against landline providers has driven prices down across the industry. Phone calls from the mobile in India are among the lowest in the world. To take the example of ownership plans for Karnataka, I pay a monthly minimum of Rs. 375 for my Vodafone connection. Calls are as cheap as 30 paise per minute. For those who use their phones less often, plans as cheap as Rs. 199 are available from Vodafone. For prepaid connections, a person needs to spend only Rs. 99 to get connected.

While the market in urban areas appears to be saturating, there is yet room for growth. This growth is likely to come in the form of more and better value-added-services (VAS). Back in 2004 people were familiar with only a handful of VAS – roaming and voicemail [2]. For long, the best that users could get were ringtones, wallpapers, themes, icons and caller tunes. Today people are not only aware but starting to use MMS, mobile web browsing, call conferencing, call forwarding, call waiting, m-banking and access other data services. India now ranks as the highest in the world for mobile data services [Mobile Web Requests India]. It is hard to believe this when my own first-hand experience does not verify it. I know people who have high-end phones with GPRS but they haven’t used GPRS yet. On the other hand, I have heard of youths in Bangalore reading blogs while they are commuting (stuck in traffic, waiting for a bus). I have heard of skilled staff (IT, telecoms, …) browsing from their mobiles in their offices where employers restrict access to many sites. If it is happening in Bangalore, it is likely to be the case in the four Metros as well.

In order to provide the higher VAS, consumer needs and behaviour must evolve. There must be a clear demand before operators and content providers can supply. We are already in the midst of this evolution in which Indian mobile culture is changing. Operators are preparing for this. 3G licences are being discussed and we may be seeing the launch of 3G in India sometime next year. It is too early to comment on this. For the moment, operators are focusing on expanding their subscriber base by providing competitive plans with low call rates and monthly rentals. VAS is not yet their priority. Likewise, content providers so far have maintained a low profile in the Indian market mainly because operators take home most of the revenue. This is unlike the market in China. Content providers in India get only 15-25 % whereas their Chinese counterparts get 85% [3].

Despite the high penetration in urban areas, ARPU (Average Revenue Per User) is quite low, one of the lowest in the world [3]. Table 2 is a comparison of EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) and ARPU [4]. If anything, ARPU is falling. For operators, this is offset by increased subscription. However, profit margins are decreasing and to stay in good shape operators have to leverage on larger economies of scale. One trend in this aspect is the sharing of towers and base station location sites among operators.

Table 2

|

|

Q2 2007 EBITDA margin

|

Q2 2006 EBITDA margin

|

Q2 2007 ARPU (in rupees)

|

Q2 2006 ARPU (in rupees)

|

|

Reliance

|

42%

|

37%

|

375

|

375

|

|

Bharti

|

41.40%

|

38.90%

|

390

|

441

|

|

IDEA Cellular

|

34.70%

|

33.70%

|

320

|

362

|

|

Spice

|

28%

|

27%

|

333

|

400

|

|

Hutchison Essar

|

—

|

33%

|

—

|

433

|

|

Source: Company financials

Information is incomplete for Hutchison Essar, which is now part of Vodafone |

There are many ways to interpret the low ARPU in India. This may have something to do with the willingness to spend from the Indian consumer. For many in the low income groups having a mobile phone is nothing more than a status symbol. They make calls only infrequently. As such, prepaid subscriptions are much more popular than postpaid. Cost for signing up is less. Incoming calls are free. BSNL has quoted that prepaid calls per day on its network is about 10 while postpaid is about 20 [5]. Data from 2004 shows that prepaid takes up two-thirds of all mobile subscriptions in the Indian market [2]. More recent data from IDC endorses the popularity of prepaid in emerging Asian markets (Bangladesh, Pakistan, Sri Lanka and Vietnam), where 95% of subscriptions are prepaid.

As an example, just two days ago I heard a first-hand account of an auto-rickshaw driver owning a prepaid mobile phone. He received an SMS in English which he didn’t understand. My friend, who was riding in his vehicle, read out the message. He needed to top-up his account. He wasn’t bothered because he could still receive calls. As another example, I had some relatives from the US who had come to Bangalore for a ten-day visit. For the duration of their stay, one of them took a prepaid subscription. Strictly speaking, she is no longer a subscriber now that she is back in the US. Likewise, it may be the case that many such prepaid connections are no longer in active use. It makes me wonder if the statistics that we see are entirely accurate. Do they reflect market penetration? Buying a subscription is one thing. Using it is another. May this be another reason for the falling ARPU?

Looking at growth potential in rural India, there is a clear case. Interest in WiMax is growing. The deployment of WiMax in India does not have a clear path yet. While ISPs are attempting to get into this space as a natural extension of their wireline broadband services, the government has left them out of initial discussions. Only cellular operators have been involved. We will need to wait and see.

While wireless to rural India will bring benefits, the nature of these benefits is not yet clear. The average rural Indian is financially a poor chap. Landowners and small-medium businesses may benefit from wireless connections but what about the landless labourer on the field? Will wireless on its own solve problems of poverty, education, water shortage and racial tensions? It is clear, in my opinion, that if wireless has to benefit rural India, a socialist model will be more appropriate than a capitalist one. A capitalist model will give wireless connectivity but will not help in attracting potential subscribers many of who are below the poverty line. Government must actively use wireless connectivity to provide remotely a host of services that would otherwise be available only in towns and cities – medical services, online education (for adults and children), e-governance (forms, birth/death certificates, marriage certificates, land registration & others), online banking and so on. An effective and viable partnership between the government and the private sector is the key to success.

The future is bright for India. Per capita income last year was about $800. Today it is around $1000. The Finance Minister has said that it will double every nine years. By 2025 it will be $4000 [6]. Urbanization of rural India is happening faster than ever before on the wave of steady economic growth. The Indian mobile market is growing and expanding in a competitive environment. It is now possible for subscribers to switch operators with the same number. The recent introduction of National Do Not Call Registry (NDNC) places consumers before intrusive marketing firms.

For long, India has been a great place for foreign companies to outsource work due to lower cost and skilled workforce. Even today, a lot of 3G and IMS specific work is done in India although their markets are elsewhere. The time has now come for the world to take notice, for the biggest market is India; and it’s growing.

References:

- Press Release No.91, TRAI, 2007.

- Vipul Chauhan, Mobile Value Chains in India, India Mobile Seminar, 2004.

- Mobile growth in India fastest, but realisations lowest, The Financial Express, Nov 21, 2005.

- Nicole Willing, Mobile Growth Blooms in India, Light Reading, Aug 03, 2007.

- Ravi Sharma, BSNL has an ambitious plan to expand customer base in State, The Hindu, Feb 17, 2007.

- India per capita income seen $1000 by ’07/08, Reuters India, Nov 5, 2007.

Read Full Post »